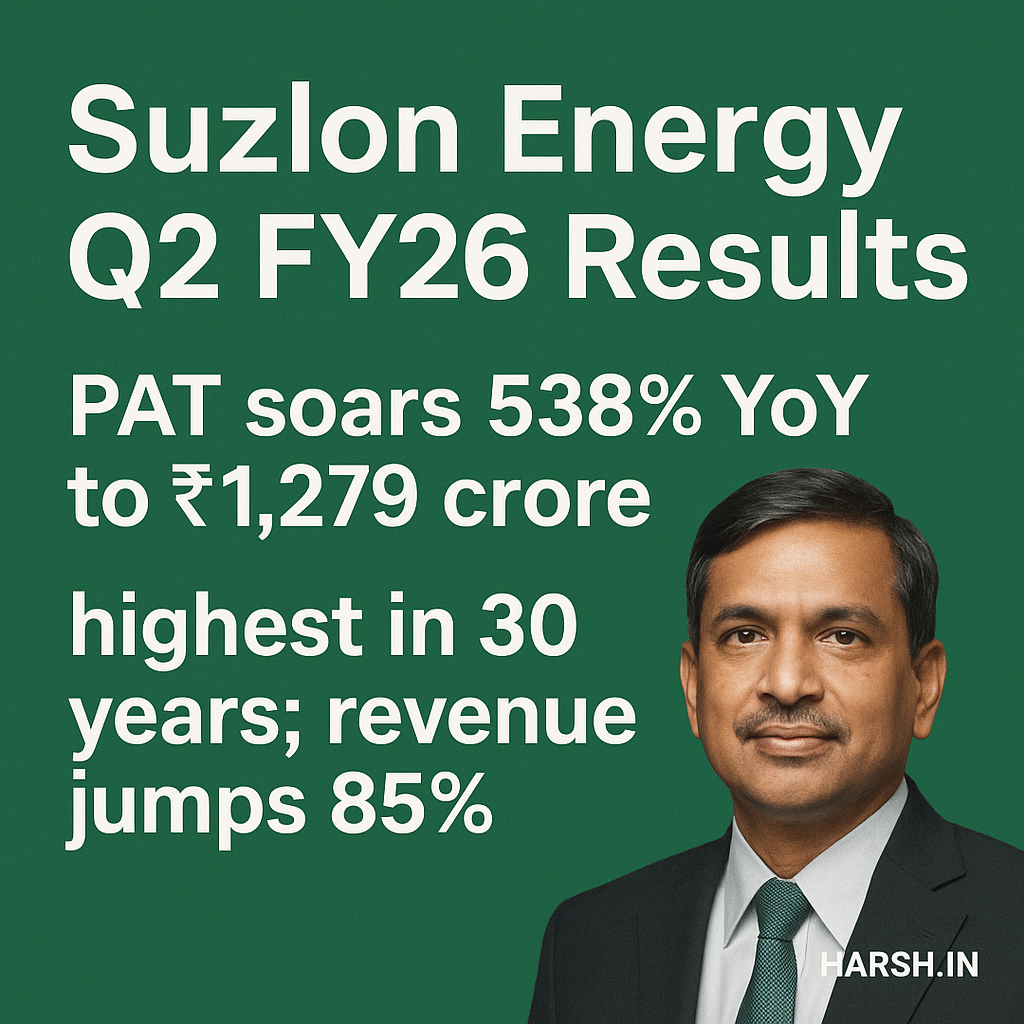

Suzlon Energy Q2 FY26 Results: PAT 538% YoY se ₹1,279 crore; Revenue 85% Jump — 30 Years ka Highest Profit

Renewable major Suzlon Energy Ltd ne Q2 FY26 (Jul–Sep 2025) me landmark performance report kiya. Company ka PAT ₹1,279 crore raha — YoY +538% — jo pichhle 30 saalon me sabse bada quarterly profit mana ja raha hai. Saath hi, revenue ~₹3,865 crore tak pahunch gaya, jo YoY ~85% ka jump dikhata hai.

Key Highlights (Point-by-Point)

Revenue Growth

Operations se revenue ~₹3,865 crore (Q2 FY26), pichhle saal ke ~₹2,093 crore se lagbhag 85% zyada.

Profit After Tax (PAT)

₹1,279 crore — YoY +538%. Is jump me deferred tax asset recognition (~₹717–₹718 crore) ka yogdan raha, jisse bottom line ko one-time boost mila.

EBITDA & Margins

EBITDA ~₹721 crore; margin ~18.6% (pichhle saal ~14.1%) — execution efficiency aur operating leverage se expansion.

Deliveries All-Time High

India me quarterly deliveries ~565 MW — company ke liye ab tak ka sabse bada quarterly volume.

Order Book Visibility

Order book ~6.2 GW cross — aane wale quarters ke liye strong pipeline ka sanket.

Balance Sheet

Net cash ~₹1,480 crore (30 Sept 2025 tak) — leverage control me, liquidity comfort improve.

Results Ko Drive Karne Wale Factors

- Execution pickup: Wind turbine generator (WTG) deliveries tezi se badhi, jisse topline aur margins dono improve huye.

- Operating leverage: Higher volumes se fixed costs spread hue, EBITDA expansion me madad mili.

- Tax impact: Deferred tax asset recognition ne PAT ko significant uplift diya — yeh recurring nahi hota.

- Policy tailwinds: India ki wind push, auctions aur localization ne demand ko support diya.

Management View (Summary)

Company ne supply-chain readiness, domestic manufacturing aur time-bound execution par focus highlight kiya. Strategy: large order book ko timely deliver karna aur service/O&M revenues ko scale karna.

What to Watch Ahead

- Order conversion & commissioning: 6+ GW pipeline ko milestones ke mutabik monetize karna.

- Input costs & logistics: Steel/components cost movement aur site logistics ka impact.

- Policy cadence: SECI/State auctions, grid evacuation readiness, manufacturing norms ki clarity.

- Margin sustainability: High base ke baad margins kaise sustain hote hain, especially bina one-offs ke.

Sector Context (Hinglish Brief)

India ka renewable build-out accelerate ho raha hai. Solar ke sath ab wind me bhi momentum pick up ho raha hai, particularly coastal & high-wind corridors me. Domestic OEMs ke liye scale + localization critical ho rahe hain — import dependence kam hoti hai, delivery reliability badhti hai.

Bottom Line

Q2 FY26 Suzlon ke liye milestone quarter raha — 30-saal ka highest profit, revenue me tez growth, deliveries record par aur order book solid. Short term me tax-related one-off ne PAT ko upar push kiya, lekin operational metrics bhi clearly improve hue hain. Aage chal kar execution aur policy cadence key monitorables rahenge.

Sources

- Economic Times – Q2 FY26 results

- Business Today – revenue & EBITDA

- Moneycontrol – deferred tax impact

- Upstox – deliveries & order book

- INDmoney – balance sheet

Disclaimer

Ye article sirf jaankari ke liye hai. Isme diya gaya content investment/financial advice nahi hai. Shares me koi bhi nirnay lene se pehle apni research karein aur registered professionals ki salah lein.